A Fragile Optimism: Small Business Sentiment Edges Down Despite Rising Wages

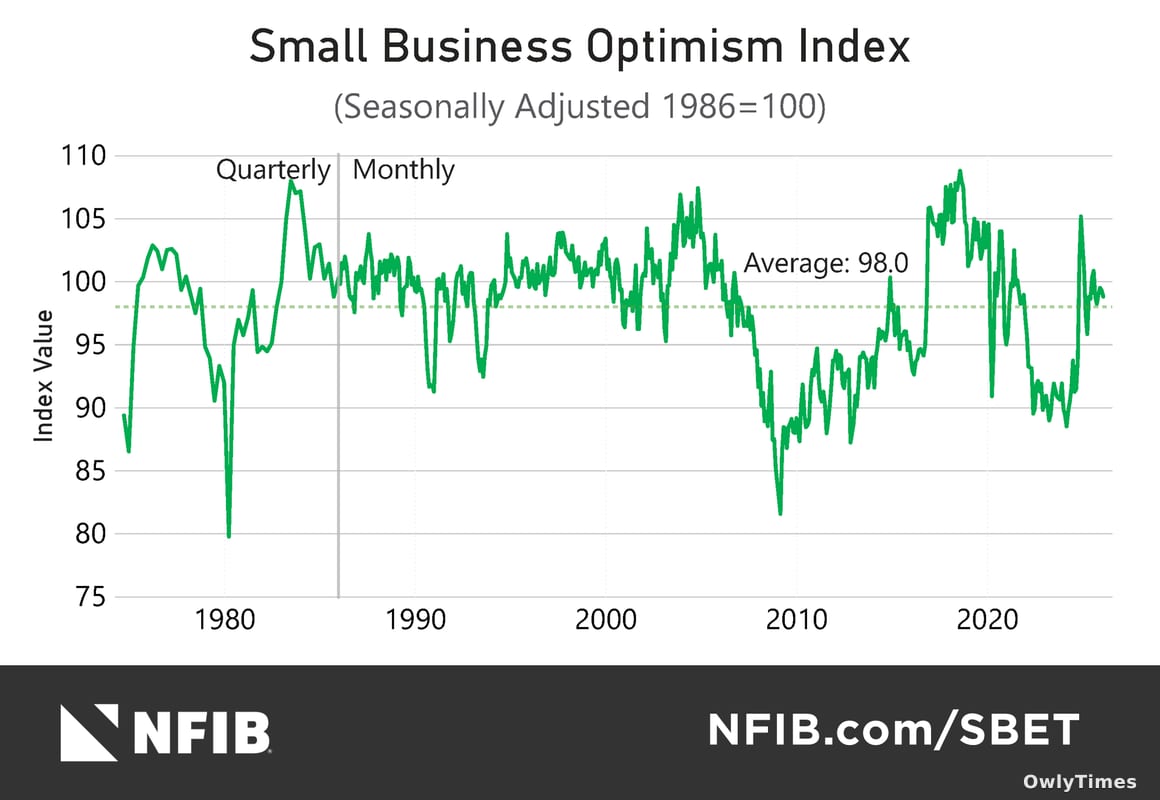

A dip to 98.8 in February – a 0.5 point decrease – might seem a minor tremor, but the latest NFIB Small Business Optimism Index signals a critical tension brewing within the Main Street economy. While still marginally above the 52-year average of 98, this decline underscores a precarious balance: small businesses are feeling slightly more confident about the future, yet simultaneously facing pressures that threaten sustained growth. Follow the money, and the story isn’t about a collapse in confidence, but a shift in the sources of that confidence – and a growing vulnerability to competitive forces.

The narrative pushed by NFIB State Director John Kabateck centers on a victory for small business advocacy, specifically the preservation of the 20% Small Business Tax Deduction. He rightly acknowledges the efforts of owners like Beth Booth of San Diego County in lobbying for this retention. However, framing the index solely through the lens of tax policy obscures a more complex reality. The deduction’s survival is a relief, certainly, but it doesn’t address the fundamental economic headwinds impacting profitability and long-term sustainability. The fact that owners are actively engaged in political advocacy suggests a proactive need to defend their interests – a sign of underlying insecurity.

Based on the original nfib.com report.

Digging into the data reveals a bifurcated picture. While optimism dipped overall, the Uncertainty Index decreased by three points to 88. This suggests owners are less anxious about unpredictable future conditions, likely fueled by a surprisingly robust February for sales and profits. A net negative 14% reported positive profit trends, a 7-point jump from January and the best result since December 2021. This is a significant improvement, indicating a short-term boost in earnings. However, this positive trend is directly juxtaposed with a concerning rise in labor costs. A seasonally adjusted 34% of owners reported raising compensation, a two-point increase from January and the highest level since March 2025. This indicates a fierce competition for workers, forcing small businesses to increase wages to remain competitive – a cost that isn’t always easily absorbed.

The slowing pace of price increases – down two points to a net 24% – is often interpreted as a sign of cooling inflation. But in this context, it’s more likely a reflection of businesses absorbing costs rather than passing them on to consumers. Bill Dunkelberg, NFIB’s Chief Economist, points to competition from larger businesses as a key stressor. This is where the vulnerability lies. Small businesses, lacking the economies of scale of their larger competitors, are less able to withstand sustained cost pressures. They can’t always raise prices without losing market share, and they’re increasingly forced to compete on labor costs, eroding their margins. The current health assessment of businesses reflects this: while 55% rate their business as “good,” a full 26% see it as “fair,” and 5% as “poor” – a baseline of fragility that could quickly worsen.

What this means for your wallet: expect continued pressure on prices, not necessarily from increases, but from a lack of downward movement. Small businesses will likely continue to absorb costs, potentially impacting investment in expansion or innovation. More importantly, watch for consolidation within industries as larger companies leverage their advantages to acquire struggling smaller firms. The question isn’t whether small business optimism will recover, but whether it can withstand the escalating competitive pressures and rising labor costs without a significant decline in overall economic health. Will the current wave of positive profit trends be enough to offset these long-term challenges, or are we witnessing a temporary reprieve before a more substantial correction?