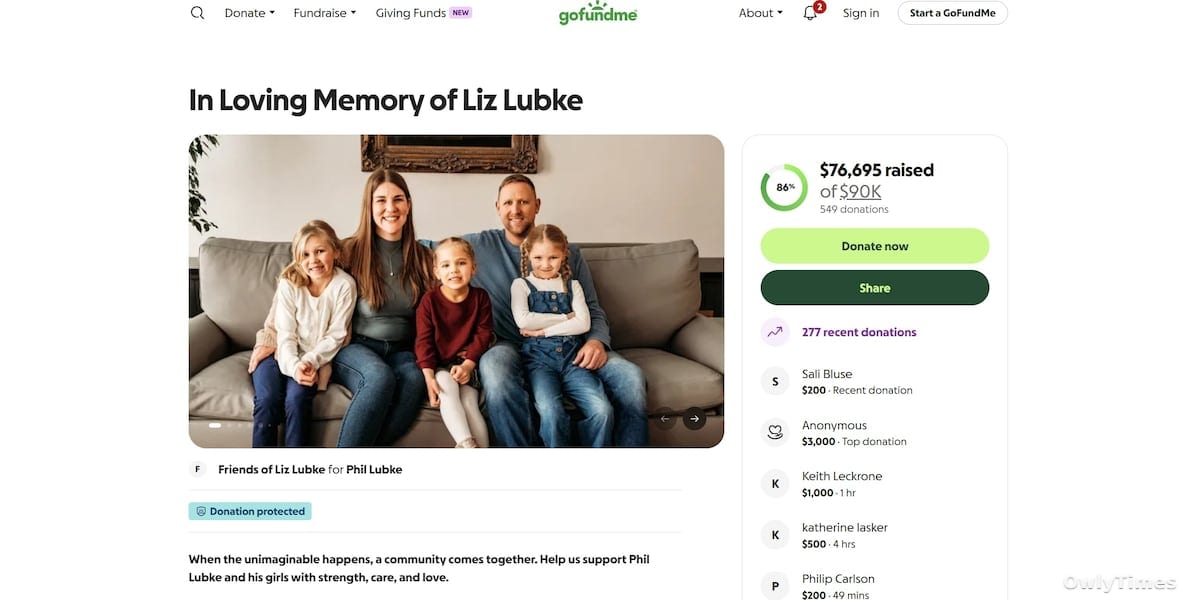

$25,000. That’s the initial fundraising goal established by the Lubke family’s support network, a figure that, while seemingly modest, underscores a critical vulnerability for small business owners facing unexpected personal tragedy. The death of Elizabeth “Liz” Lubke, 39, of Eau Claire, Wisconsin, following a multi-vehicle collision in Kentucky on March 28th, isn’t simply a local tragedy; it’s a stark illustration of the financial fragility woven into the fabric of the American entrepreneurial landscape. While the immediate focus is rightly on supporting the Lubke family – her husband and three daughters, including one airlifted to a pediatric level-1 trauma center – the circumstances surrounding her death reveal a pattern of risk often overlooked when celebrating small business success.

The Hidden Costs of Sole Proprietorship

Lubke owned and operated E.L. Pilates, a business dedicated to injury recovery and chronic pain management. The GoFundMe page established to aid the family explicitly highlights this aspect of her work, emphasizing her dedication to helping others heal. This detail is crucial. Unlike employees with employer-sponsored benefits, sole proprietors like Lubke are entirely responsible for their own insurance coverage – health, disability, and business interruption. A 2023 study by the Kaiser Family Foundation found that self-employed individuals are 15% less likely to have health insurance than those with traditional employment, and even fewer carry adequate disability coverage. The $25,000 goal, while intended to cover immediate medical and logistical expenses, likely represents only a fraction of the long-term financial impact of losing both a primary income earner and the owner of a small business.

Drawn from weau.com.

Kentucky Collision, Wisconsin Impact

The collision itself, involving three vehicles in Christian County, Kentucky, according to a press release from the Kentucky State Police, highlights the unpredictable nature of risk. While investigations are ongoing, the incident underscores the vulnerability of families traveling – a common occurrence for small business owners seeking respite. Lubke was en route to Alabama with her family for spring break when the crash occurred. The airlift to a Tennessee hospital, followed by her death on March 30th, adds layers of complexity to the financial burden. Air ambulance services are notoriously expensive, often exceeding $50,000 per flight, and are frequently not fully covered by insurance. This expense, coupled with ongoing medical bills for her daughter and the loss of Lubke’s income, creates a cascading financial crisis for the family.

Beyond the Business: Community and Civic Capital

The outpouring of support from the Eau Claire community – a GoFundMe and a meal train – speaks to Lubke’s active involvement beyond her business. Her dedication to Longfellow Elementary’s PTO and advocacy for the school’s dual immersion Spanish language program demonstrate a significant investment of social capital. This isn’t merely anecdotal; research consistently shows a correlation between community involvement and small business success. A 2022 study by the Small Business Administration found that businesses with strong community ties are 20% more likely to survive their first five years. The loss of Lubke represents a loss not just to her family, but to the civic fabric of Eau Claire itself. The financial strain on the family could also limit their ability to continue this community engagement, creating a ripple effect.

What This Means for Your Wallet

The Lubke family’s situation is a cautionary tale for both entrepreneurs and consumers. For those considering starting a small business, it’s a critical reminder to prioritize comprehensive insurance coverage – not just for the business itself, but for personal health and disability. Don’t underestimate the potential financial devastation of an unexpected event. For consumers, supporting local businesses isn’t just about economic stimulus; it’s about recognizing the inherent risks faced by these entrepreneurs and acknowledging the potential for unforeseen circumstances. Consider direct support mechanisms like GoFundMe campaigns, but more importantly, advocate for policies that provide a stronger safety net for self-employed individuals. The question now is: will the insurance industry and policymakers respond to the growing precarity of the self-employed, or will more families find themselves facing similar financial hardship in the wake of personal tragedy?