The expiration of enhanced Affordable Care Act (ACA) marketplace subsidies at the end of 2025 isn’t simply a policy lapse; it’s a revealing stress test of the American healthcare system, and the results are beginning to come in. While headlines focus on premium increases – and the dramatic doubling estimated by the KFF (Kaiser Family Foundation) for the average recipient – the real story is the cascading series of financial compromises now facing millions, and the political fault lines exposed by the shift. It’s not just about higher monthly bills, but about access, coverage levels, and a growing sense of precarity for those relying on the ACA as a safety net.

The enhanced subsidies, enacted in 2021, demonstrably lowered the cost of insurance for roughly 22 million people – over 90% of all ACA enrollees – last year. Their absence isn’t a gradual increase in cost, but a sharp cliff edge. For families like Nancy Linder and her husband outside Atlanta, premiums have tripled, jumping from $162 to $483 per month – a nearly $3,900 annual burden on a $30,000 income. This isn’t an isolated case. Kate Bivona and her husband in Arizona were forced to downgrade from a silver-tier plan to a bronze plan, accepting a $15,000 deductible in exchange for a marginally lower monthly premium. And others, like Robin Wright-Pierce and her husband in Cincinnati, have been forced to drop coverage altogether. These aren’t abstract economic figures; they are real people making agonizing choices between healthcare and other essential needs.

The political implications are equally stark. Despite Republican opposition to extending the subsidies, data from KFF reveals a surprising trend: 88% of ACA enrollment growth since 2020 – 11.9 million new enrollees – occurred in states won by President Donald Trump in the 2024 election. This suggests the subsidies weren’t simply benefiting traditionally Democratic constituencies, but were actively expanding access in areas where the need was demonstrably present. The White House, through spokesman Kush Desai, downplays the impact, framing the affected population as a “relatively small share” and touting President Trump’s “Great Healthcare Plan.” However, this statement sidesteps the immediate and tangible hardship experienced by millions, and ignores the political resonance of those hardships. The administration’s focus on future plans doesn’t address the current crisis unfolding for ACA enrollees.

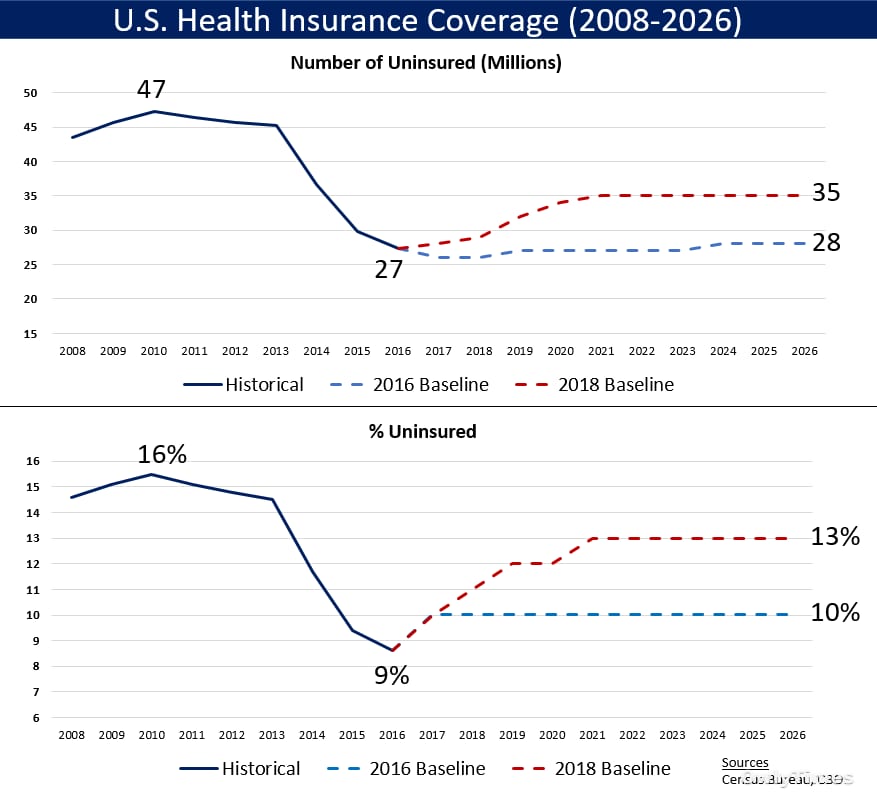

The ACA marketplace was originally designed as a last resort for those unable to access insurance through employers, Medicare, or Medicaid. It serves a crucial population: small business owners, gig workers, freelancers, and early retirees. The current situation highlights the fragility of this system and the extent to which affordability is the primary barrier to access. While the federal government continues to provide baseline premium tax credits, the re-emergence of the “subsidy cliff” – disqualifying households earning just above 400% of the federal poverty line – has created a new class of uninsured, even among those who previously qualified for assistance. The story of Wright-Pierce and her husband exemplifies this, demonstrating how a modest income increase can suddenly render healthcare unaffordable.

Original reporting: CNBC.

It’s important to acknowledge the limitations of drawing broad conclusions from these individual stories. They represent a snapshot of the impact, and may not be fully representative of the entire ACA marketplace. Early state-level data from California and Pennsylvania, however, corroborate the trend of downgrades to bronze plans, with a 30% increase in bronze enrollment in Pennsylvania and a shift to 29% bronze enrollment in California. Furthermore, estimates from the Urban Institute suggest that as many as 5 million people could lose ACA coverage in 2026. These figures, combined with the personal accounts, paint a concerning picture.

Looking ahead, the critical question isn’t simply whether the subsidies will be reinstated, but how to address the underlying structural issues that make healthcare affordability so precarious. Will Congress revisit the subsidy cliff? Will alternative solutions, such as expanding Medicaid or implementing a public option, gain traction? The next phase of research needs to focus on tracking the long-term health outcomes of those who have lost coverage or downgraded their plans. Are we seeing an increase in delayed care, preventable hospitalizations, or medical debt? And, crucially, how will these changes impact voter behavior in the upcoming elections? The fate of the ACA, and the health security of millions of Americans, hangs in the balance.