The Inland California Distress Signal: A $39 Billion Problem

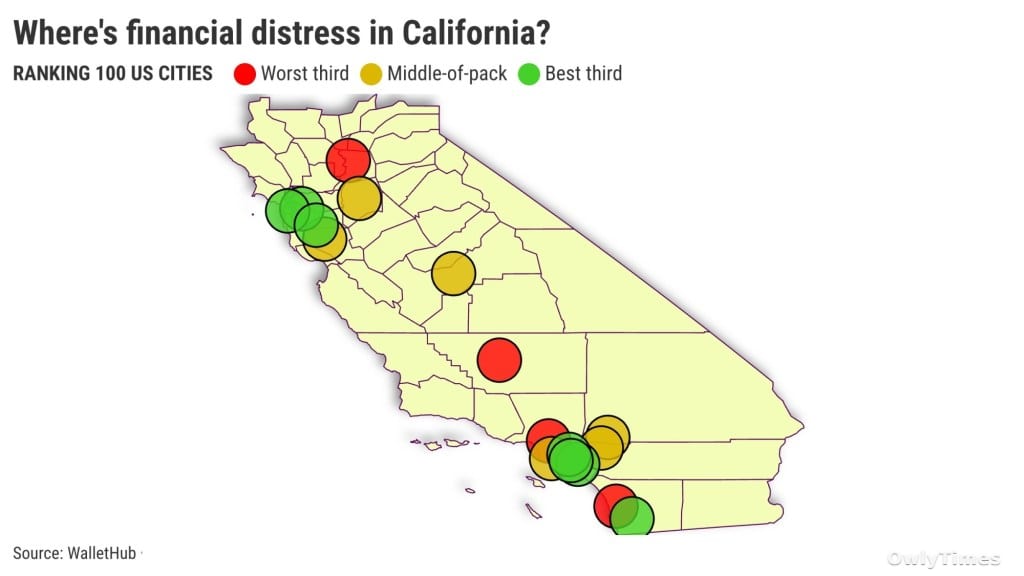

A composite ranking of financial distress across 100 U.S. cities places inland California at a significantly higher risk than its coastal counterparts – averaging a 39th-worst national ranking, translating to roughly $39 billion in potential economic friction across just six cities. This isn’t a story about California’s famed affordability solving all problems; it’s a data-driven illustration of how wage stagnation inland creates a persistent vulnerability, even where housing costs are lower. Jonathan Lansner’s analysis, based on a WalletHub ranking incorporating credit scores, late payments, bankruptcies, and online debt searches, reveals a geographic divide in financial health that demands closer scrutiny.

Source material: mercurynews.com.

The headline figure – 39th – isn’t simply a number; it represents a systemic weakness. To put this in perspective, the seven cities of Southern California averaged a 56th-worst ranking, while the four cities in the Bay Area clocked in at 69th. This 20-point gap between inland California and the Bay Area alone suggests a fundamental economic divergence. Bakersfield leads the inland distress, landing at 24th nationally, followed by Sacramento (30th), San Bernardino (39th), Stockton (43rd), Fresno (45th), and Riverside (52nd). These aren’t isolated incidents; they’re interconnected points on a map of economic pressure.

The Credit Score Divide and the Rising Tide of Late Payments

Digging into the data, the root of the problem isn’t a single factor, but a confluence of vulnerabilities. Credit scores are demonstrably lower inland, a critical indicator of access to capital and the cost of borrowing. This isn’t merely a correlation; lower wages inland directly impact the ability to maintain good credit, creating a vicious cycle. Equally concerning is the prevalence of late payments, also concentrated inland. While Southern California shows some resilience in this area, the inland cities consistently report higher rates of delinquent bills. This suggests a struggle to meet even basic financial obligations, a warning sign for broader economic stability. The data shows late payments are least common in Northern California, a region benefiting from the tech boom and higher average incomes.

Los Angeles: An Outlier of Coastal Distress

While the inland-coastal divide is the dominant narrative, Los Angeles’ ranking as the fifth-worst nationally for financial distress throws a wrench into the simple geographic explanation. With a population of nearly 4 million, Los Angeles’ struggles aren’t just a local issue; they represent a significant drag on the state’s overall economic health. San Diego (22nd) and Long Beach (48th) also contribute to Southern California’s comparatively weaker performance, demonstrating that even coastal cities aren’t immune to financial pressures. This highlights the importance of looking beyond broad regional trends and examining individual city dynamics. The concentration of high-cost housing in these areas, coupled with income inequality, appears to be a key driver of distress.

Bankruptcy Trends: A Slow Burn Inland, Stability Down South

The bankruptcy filing data offers a nuanced picture. While bankruptcies are increasing inland, the rate of growth is slowest in Southern California. This suggests that while inland cities are already experiencing financial hardship, Southern California is potentially building towards future problems. The Bay Area, with its robust economy, shows the lowest bankruptcy rates overall. This isn’t necessarily a sign of economic perfection, but rather a reflection of higher incomes and a stronger social safety net. Online searches for debt and loans, another key metric, also confirm the inland trend, with residents in these areas more frequently seeking financial assistance.

What This Means for Your Wallet

The WalletHub data isn’t just an academic exercise; it has tangible implications for consumers and investors. If you’re considering relocating to inland California for affordability, understand that lower housing costs may be offset by limited job opportunities and a higher risk of financial instability. For investors, this data suggests that inland California may present both challenges and opportunities. While distressed markets can offer potential for high returns, they also carry increased risk. Watch for a potential increase in loan defaults and bankruptcies in inland California cities over the next 12-18 months, particularly if economic conditions worsen. The question now is: will targeted economic development initiatives be enough to mitigate these risks, or will the inland-coastal financial divide continue to widen?