$150 Oil: The Invisible Hand Restraining US Foreign Policy

A 21% surge in Brent crude oil prices since February 27th, 2026 – exceeding the rate observed during the initial weeks of the Ukraine war – is quietly dictating the boundaries of the Trump administration’s response to escalating tensions with Iran. While geopolitical rhetoric focuses on potential military action, a closer examination of market behavior reveals financial stability concerns are rapidly becoming the primary constraint on US policy, effectively forcing a recalibration of strategy. This isn’t about diplomatic restraint; it’s about the bond market.

The historical record is stark. In April 2025, a nearly 150% tariff hike on Chinese goods triggered a crisis in the US Treasury market, compelling a policy reversal. Again, in January 2026, a global spike in government bond yields coincided with a strategic retreat regarding Greenland. These weren’t isolated incidents, but rather demonstrations of a consistent pattern: financial markets act as a hard limit on presidential ambition. The precedent of March 2020, when a collapse in oil prices sparked global turmoil and necessitated massive Federal Reserve quantitative easing (QE), underscores this dynamic. The current oil price trajectory, therefore, isn’t simply an energy issue – it’s a systemic risk indicator.

Options Markets Signal Mounting Fear

The shift in market sentiment over the past week is particularly telling. While spot markets – where direct oil purchases occur – show concerning trends, the real alarm bells are ringing in options markets. These markets, used for hedging against uncertainty, are experiencing far more violent swings than their spot counterparts. This indicates investors are bracing for a far more significant disruption than directional oil traders are currently pricing in. Implied volatility, a measure of expected price fluctuations, is rising across multiple asset classes: the S&P 500, the bond market (as measured by the MOVE index), and high-yield corporate debt are all signaling increased demand for protection. This isn’t a measured response to geopolitical risk; it’s a scramble for insurance.

This article draws on reporting from substack.com.

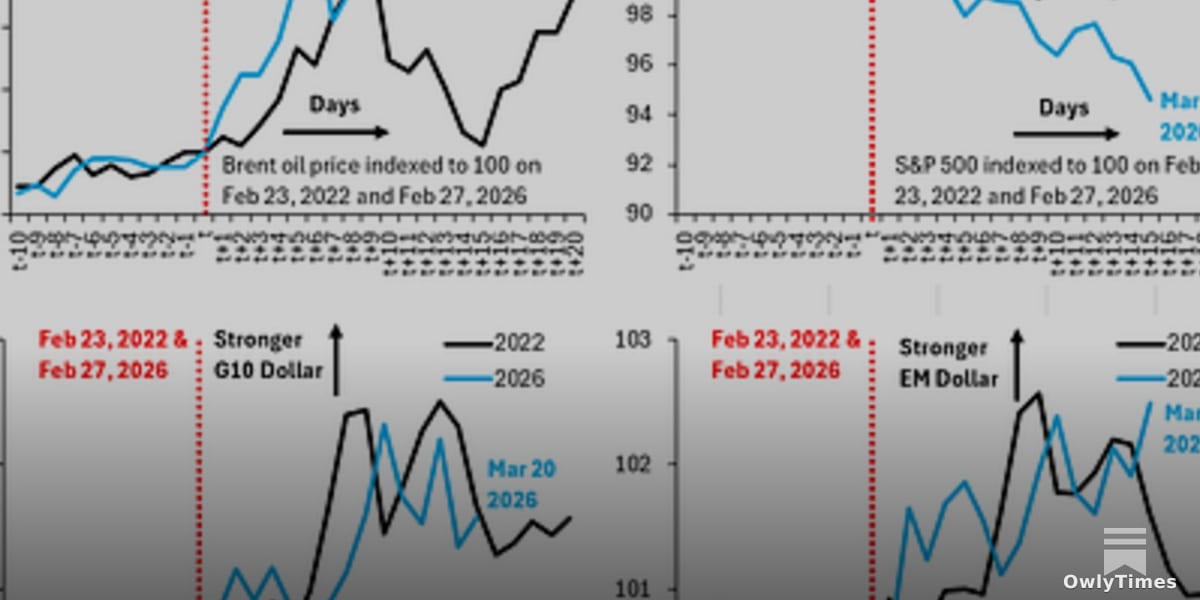

Comparing current market conditions to February 2022, the data paints a grim picture. Indexed to the day before the Ukraine invasion, Brent crude, the S&P 500, and emerging market currencies are all performing worse now than they were during the initial stages of that conflict. While movements remain orderly for now, the direction is unequivocally negative. This suggests the market is already factoring in a substantial risk premium, anticipating further escalation and potential economic fallout. The fact that options markets are reacting more strongly than spot markets suggests the perceived tail risk – the possibility of a catastrophic event – is significantly higher.

The Kharg Island Calculation: A Financial Constraint

This heightened financial fragility explains why, according to analysis, the Trump administration is increasingly likely to pursue a “mission accomplished” narrative rather than risk further escalation, specifically regarding potential military action targeting Kharg Island, a key Iranian oil terminal. A successful strike on Kharg Island would almost certainly trigger a massive spike in oil prices, potentially exceeding the levels seen in 1979. Such a shock could overwhelm global financial systems, triggering a cascade of defaults and liquidity crises.

Paul Krugman, in a recent discussion, echoed this sentiment, suggesting oil prices are nearing their peak, in part due to the administration’s awareness of market vulnerabilities. While this assessment offers a degree of optimism, it’s crucial to recognize the inherent uncertainty. The current situation is a delicate balancing act, where geopolitical objectives are being actively constrained by the invisible hand of the market. The administration’s willingness to de-escalate isn’t necessarily a sign of strength, but rather a pragmatic response to a looming financial threat.

What This Means for Your Wallet

The implications for consumers and investors are significant. Higher oil prices translate directly into increased energy costs, impacting everything from gasoline at the pump to heating bills. More broadly, sustained high oil prices contribute to inflationary pressures, eroding purchasing power and potentially triggering further interest rate hikes. Investors should brace for increased market volatility and consider diversifying portfolios to mitigate risk. The key question now isn’t if the market will react to further escalation, but how severely. Watch closely for a sustained breach of $175 per barrel for Brent crude – that level would likely signal a breaking point, forcing the Fed to intervene and potentially triggering a broader financial crisis.